Cost management planning activity defines policies and procedures to plan, manage and control costs on the project. This helps you create the Cost Management plan, which is part of the Project Management plan.

Cost management planning activity defines policies and procedures to plan, manage and control costs on the project. This helps you create the Cost Management plan, which is part of the Project Management plan.

This is not a process that is often executed, once at the beginning of the planning phase of the project and then at preplanned intervals such as the beginning of a new phase.

What do you need to create the Cost Management Plan?

In order to estimate costs you need to know how schedule and risks are managed on the project. Simply because schedule and risks are two areas that can shoot your project costs out of the roof if not managed properly.

The 2 documents that tell you how they are managed – that is, schedule management plan and the risk management plan – are part of the Project management plan.

The information used from these are – scope baseline and schedule baselines primarily, and then other relevant information such as risks and communication needs related to cost management.

Project charter contains summary budget information and budget approval needs which are essential.

Apart from these, you’ll also be referring to the published industry specific labor rates, project management information systems, and lessons learned while managing costs in other earlier projects, any templates and policies governing cost management specific to the organization, financial knowledge bases and so on.

If your costs are based on procurement from vendors and suppliers, the type of contract you’ll have with them will also have a bearing on your overall cost planning. Plus, if there are imports involved then currency fluctuation is something to be considered as well.

These are all part of EEF and OPA.

How do you do it?

In most cases experts sit together and create the Cost management plan based on their experience – either from other similar projects in the organization, or from their own experience in the past.

In some cases analytical techniques such as payback period, return on investment (ROI), internal rate of return, discounted cash flow and net present value are used.

Funding considerations are thought through – whether the project will be funded from the banks, self-funded, funded with equity or debt, and so on. Certain alternatives such as buy-make-lease can have detrimental impact on costing, and this is analyzed as well.

Certain decisions such as project funding and ways to finance project resources decide which of these techniques to be used. Some of the alternatives available for project funding are funding with equity, funding with debt and self-funding. Resources can be rented, leased, purchased or made in-house.

Cost Management Plan

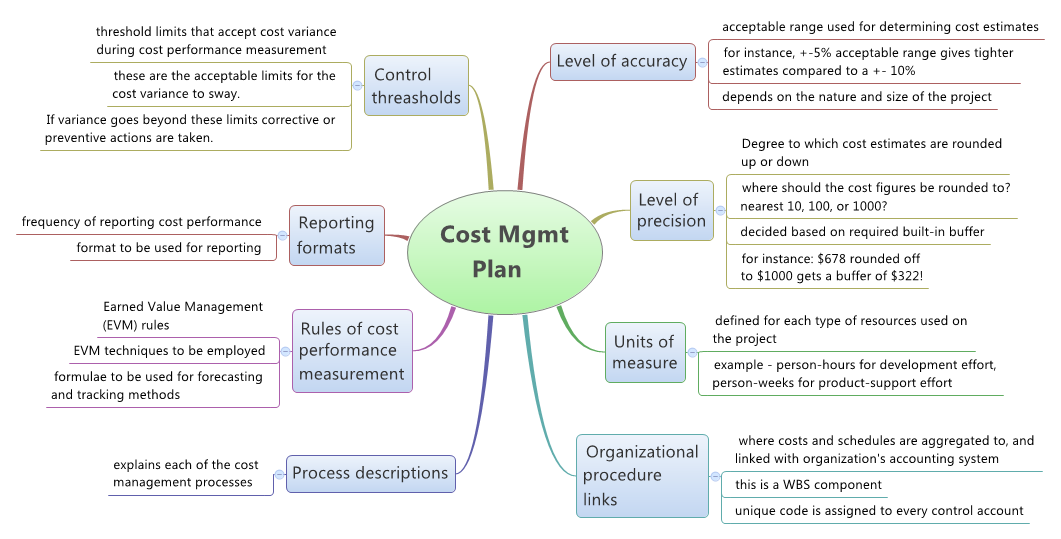

Following mind map is self-explanatory and shows the contents of Cost management plan and their purposes. Click to open in a new window.

Figure: The cost management plan

Figure: The cost management plan

Some of the information covered in the cost management plan are –

- Level of accuracy – acceptable range used for determining cost estimates. For instance, +-5% acceptable range gives tighter estimates compared to +-10% – but it comes at additional time and cost.

- Level of precision – the degree to which cost estimates are rounded up or (ceiling) down (floor). Decide whether the figure should round up to nearest 10, 100, or 1000. This decision is guided by the in-built buffer you need.

- Unit of measure used for cost calculations – defined for each type of resource used on the project. Example, person-hr for development effort, and person-weeks for product design effort.

- Rules of performance measurement – Earned Value Management rules used for this project, techniques to be used, and formula to be used for forecasting and tracking, and so on.

- Cost reporting formats – frequency and format of reporting, determined by stakeholder communication needs as well!

- Control thresholds – Threshold limits that accept cost variance during cost performance measurement. If variance goes beyond these limits then corrective or preventive actions are taken.

- Process description – of course, based on tailoring considerations the processes and their descriptions are mentioned as well.

So, that’s about cost planning. Though the process itself seems simple, execution can be quite tricky. This is usually done in multiple iterations so as to come up with a plan that is just right in terms of effort and returns on that effort.

Next, let us see how the biggie is done – Estimating project cost!